Breaking Down Credit Card Machine Percentages: A Guide

When it comes to managing a small business in the U.S., understanding the credit card machine percentage is crucial for optimizing profits and ensuring seamless operations. At its core, this percentage represents the fees charged on each credit card transaction, typically ranging from 1.5% to 3.5% of the sales amount. These fees include:

Interchange fees: Paid to the bank that issued the customer's card.

Assessment fees: Paid to the card network (like Visa or Mastercard).

Payment processor fees: Paid to the company that handles the transaction processing.

Navigating these fees can be complex, but it's essential for reducing costs and enhancing the customer experience. As a small business owner, knowing the breakdown of these percentages can help you select the right payment processor and pricing model to minimize expenses.

I'm Lydia Valberg, and I've been committed to providing transparent and effective payment solutions for over three decades. My experience with credit card machine percentage, coupled with my dedication to excellent customer service, has helped many businesses like yours thrive by optimizing transaction-related costs.

Understanding Credit Card Machine Percentages

When you make a sale using a credit card, a small portion of that transaction goes toward various fees. This is what we call the credit card machine percentage. Let's break it down:

Processing Fees

These are the costs associated with handling each credit card transaction. Think of them as the price you pay for the convenience of accepting card payments. Typically, these fees are a combination of different charges, including interchange fees and assessment fees.

Discount Rate

The discount rate is the total percentage of a credit card sale that a merchant pays in fees. For example, if your discount rate is 2% and you make a $100 sale, $2 goes toward fees. This rate is crucial because it directly affects your profit margin. Understanding your discount rate helps you plan and price your products accordingly.

Interchange Fees

Interchange fees are paid to the bank that issued the customer's card. These fees vary based on several factors, such as the type of card used and the transaction method. For instance, debit cards often have lower interchange fees compared to credit cards.

Understanding these components can help you make informed decisions about which payment processors and pricing models best suit your business needs. By watching your credit card machine percentage, you can minimize costs and improve your bottom line.

Next, we'll explore the components of credit card processing fees to give you a clearer picture of where your money goes and how you can potentially save.

Components of Credit Card Processing Fees

When it comes to understanding the credit card machine percentage, break down the components involved in credit card processing fees. These fees are not just a single charge; they consist of several parts, each playing a role in the transaction process.

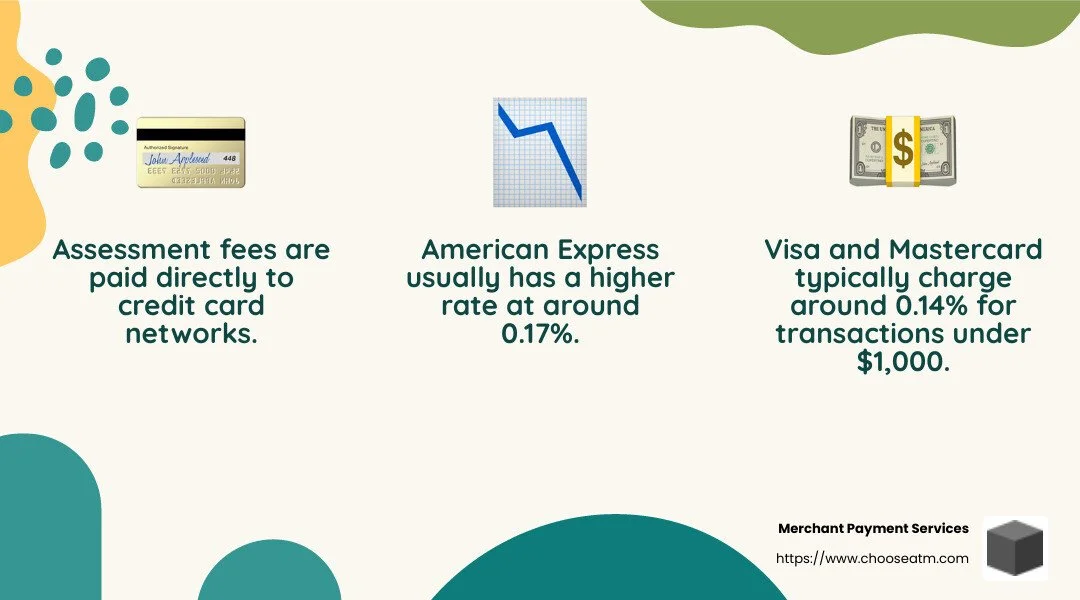

Assessment Fees

Assessment fees are a small part of the overall transaction cost, but they are vital. These fees are paid directly to the credit card networks like Visa, Mastercard, Find, and American Express. Each network sets its own rates, which can vary slightly. For example, Visa and Mastercard typically charge around 0.14% for transactions under $1,000. In contrast, American Express tends to be a bit higher at 0.17%.

These fees help cover the operating costs of the networks and ensure secure transactions. Though they are a minor part of the total, they are unavoidable and non-negotiable.

Interchange Fees

Interchange fees are the largest component of the credit card processing fees. These are paid to the bank that issued the customer's card. The rates can vary widely depending on the type of card and how the transaction is processed. For example, credit cards generally have higher interchange fees than debit cards.

Interchange fees are calculated as a percentage of the transaction plus a fixed amount. For instance, a typical fee might be 1.5% of the transaction plus 10 cents. These fees compensate the issuing bank for the risk and cost of offering credit to the cardholder.

Payment Processor Fees

Payment processor fees are charged by the company that handles the logistics of processing each transaction for your business. This includes companies that provide the technology and services to ensure that payments are processed smoothly and securely.

These fees can often be negotiated, depending on your transaction volume and the processor you choose. Some processors offer flat rates, while others use a tiered or interchange-plus model. For example, with the interchange-plus model, you might pay a consistent markup, such as 0.4% plus 8 cents, in addition to the interchange fees.

Understanding these components is crucial for managing your credit card machine percentage effectively. By knowing where each fee goes, you can better assess your payment processing needs and potentially negotiate lower rates with your processor.

Next, we'll dive into the different pricing models for credit card processing to help you choose the best option for your business.

Pricing Models for Credit Card Processing

When it comes to managing your credit card machine percentage, choosing the right pricing model is key. Here's a breakdown of the three main models: tiered pricing, flat-rate pricing, and interchange-plus pricing.

Tiered Pricing

Tiered pricing is like a menu with different options. It categorizes transactions into three tiers: qualified, mid-qualified, and non-qualified.

Qualified Tier: This includes basic debit and credit cards without rewards. It's the cheapest tier.

Mid-Qualified Tier: This tier covers credit cards with certain rewards programs. It's more expensive than the qualified tier but cheaper than the non-qualified tier.

Non-Qualified Tier: This is the priciest tier, often including corporate cards and cards with big rewards.

With tiered pricing, the cost to process a transaction depends on the tier the card falls into. While it might offer lower costs for some transactions, it can be tricky to predict your total fees.

Flat-Rate Pricing

Flat-rate pricing is straightforward. You pay a single, consistent rate for all transactions. This model is popular for its simplicity and predictability.

Predictable Costs: You always know what you'll pay, regardless of the card type or transaction size.

No Surprises: Ideal if you want to avoid unexpected fees.

However, flat-rate pricing might not be the cheapest option. You can't lower your costs by favoring certain card types, as you can with tiered pricing.

Interchange-Plus Pricing

Interchange-plus pricing is a transparent model. You pay the actual interchange fee plus a fixed markup.

Transparency: You see exactly what you're paying for the interchange fee and the processor's markup.

Potential Savings: By always getting the lowest interchange fee, you might save money compared to flat-rate pricing.

This model is great for businesses that want clarity and the potential to save on processing fees.

Choosing the right pricing model can significantly impact your credit card machine percentage. Each model has its pros and cons, so consider your business needs and transaction volume when deciding. Next, we'll explore how to minimize these percentages further.

How to Minimize Credit Card Machine Percentages

Reducing your credit card machine percentage can boost your bottom line. Here are three key strategies to help you keep those fees in check:

Surcharging

Surcharging is when you pass the credit card processing fee to your customers. This means adding a small fee when a customer chooses to pay with a credit card.

Legal Considerations: Before implementing surcharging, check your state laws. Some states, like Connecticut, have specific regulations about surcharging.

Customer Transparency: Always make sure the surcharge is clearly displayed to customers before they pay. This transparency helps maintain trust.

Fee Negotiation

Negotiating with your payment processor can lead to lower fees. Here’s how you can make a strong case:

Transaction Volume: If your business processes a high number of transactions, use this as leverage. More transactions can mean more negotiating power.

Shop Around: Don’t settle for the first offer. Compare different processors and use their offers to negotiate better terms.

Understand Your Statement: Know the breakdown of your fees. This knowledge empowers you to ask for specific reductions.

Payment Processor Selection

Choosing the right payment processor is crucial. Here’s what to consider:

Transparent Pricing: Look for processors with clear, transparent pricing. Avoid those with hidden fees or complicated contracts.

Customer Support: Good support can save you time and money. Choose a processor known for excellent customer service.

Scalability: As your business grows, your needs will change. Pick a processor that can scale with you.

By implementing these strategies, you can effectively reduce your credit card machine percentage and improve your profit margins. Next, we'll address some common questions about these percentages.

Frequently Asked Questions about Credit Card Machine Percentages

What is the average credit card machine percentage?

The credit card machine percentage typically ranges from 1.5% to 3.5% of the total transaction. This percentage includes various fees such as interchange fees, assessment fees, and payment processor fees. It's important to understand these components to know exactly what you're paying for each transaction.

Is it legal to charge a surcharge on credit card transactions?

Charging a surcharge on credit card transactions is legal in many states, but not all. For example, Connecticut and Massachusetts have laws prohibiting surcharges. Always check your state's regulations before implementing a surcharge policy. Transparency is key—make sure your customers are aware of any additional charges before they complete their purchase. This not only maintains trust but also complies with consumer protection laws.

How do credit card machine percentages impact small businesses?

For small businesses, credit card machine percentages can significantly affect profit margins. These fees are often unavoidable, but they do add up. High transaction fees can eat into profits, especially for businesses with lower sales volumes.

To manage these costs, small businesses can explore options like negotiating fees with payment processors or considering a two-tier pricing system where credit card and cash prices are displayed separately. This helps in maintaining competitive pricing while covering the costs associated with credit card transactions.

By understanding and managing these fees, small businesses can protect their bottom line and ensure healthier profit margins.

Next, we'll wrap up with a look at how Merchant Payment Services can help you maximize your cash flow and reduce processing fees.

Conclusion

At Merchant Payment Services, we understand that managing credit card processing fees is crucial for any business. These fees can significantly impact your bottom line, especially if you're a small business. That's why we're committed to helping you maximize cash flow and reduce processing fees.

With over 35 years of experience, we're experts in simplifying ATM ownership and management. Our services not only offer access to leading ATM brands like Nautilus Hyosung and Genmega but also help in reducing credit card processing fees. By partnering with us, you can improve your profits through surcharge revenue and increased foot traffic, all while keeping your transaction costs in check.

Our unique approach focuses on delivering custom solutions that meet your specific needs. We believe that every business deserves to thrive without the burden of excessive fees. Our expertise in ATM management and credit card processing allows us to provide you with the tools and support you need to manage your business finances effectively.

For more information on how we can assist you in optimizing your payment processes and boosting your profits, visit our service page.

Let Merchant Payment Services be your trusted partner in navigating the complexities of credit card processing and achieving financial success.